Last In, First Out LIFO: The Inventory Cost Method Explained

Inventory management software and processes allow for real-time updating of the inventory count. Often, this means employees use barcode scanners to record best freelance services in 2021 sales, purchases or returns at the moment they happen. Employees feed this information into a continually adjusted database that tracks each change.

How To Calculate Ending Inventory and COGS Using the LIFO Method

Under LIFO, you’ll leave your old inventory costs on your balance sheet and expense the latest inventory costs in the cost of goods sold (COGS) calculation first. While the LIFO method may lower profits for your business, it can also minimize your taxable income. As long as your inventory costs increase over time, you can enjoy substantial tax savings. In a perpetual inventory system, FIFO (First-In, First-Out) and LIFO (Last-In, First-Out) are methods used to track inventory and cost of goods sold (COGS). FIFO assumes that the oldest inventory items are sold first, so COGS reflects the cost of older inventory. Conversely, LIFO assumes that the newest inventory items are sold first, so COGS reflects the cost of newer inventory.

3 Calculate the Cost of Goods Sold and Ending Inventory Using the Perpetual Method

Second, we need to record the quantity and cost of inventory that is sold using the LIFO basis. She launched her website in January this year, and charges a selling price of $900 per unit. If you’re new to accountancy, calculating the value of ending inventory using the LIFO method can be confusing because it often contradicts the order in which inventory is usually issued.

- The real value of perpetual inventory software comes from its ability to integrate with other business systems.

- This means that COGS and ending inventory are calculated only at the end of the period.

- Try FreshBooks for free to boost your efficiency and improve your inventory management today.

- This system continuously updates inventory records as transactions occur, providing businesses with accurate information on their available stock at any given time.

Periodic Inventory System

The retail sales for this product in this company were $25,000 from Jan. 1, 2019 to Jan. 15, 2019. In this section, we will discuss some of the key formulas used in perpetual inventory systems to help businesses effectively manage their stock levels and make informed decisions. These formulas include COGS, economic order quantity (EOQ), weighted average cost, and gross profit.

Description of Journal Entries for Inventory Sales, Perpetual, First-in, First-out (FIFO)

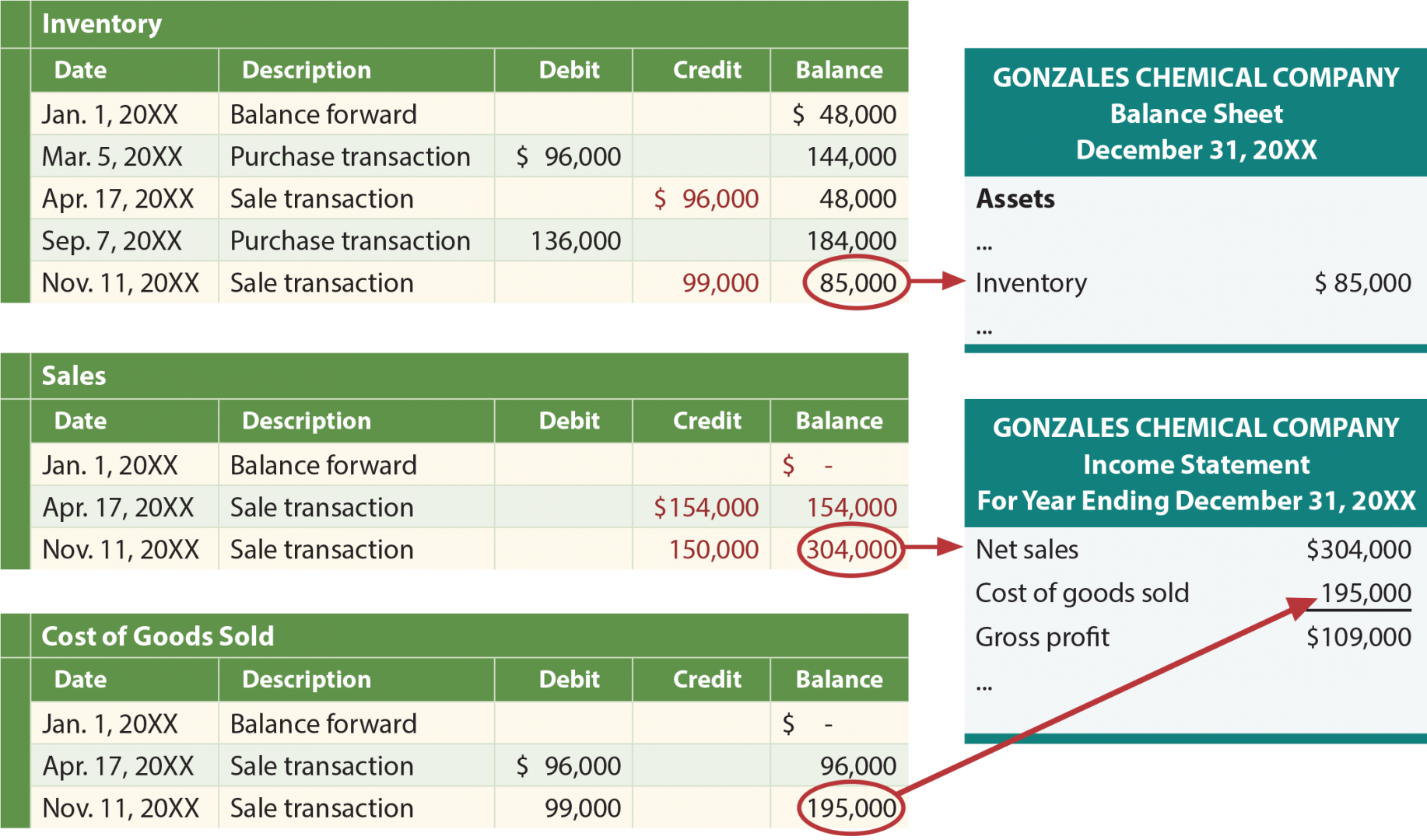

A perpetual inventory system is an advanced method of tracking and managing the stock levels of goods in real time. This system continuously updates inventory records as transactions occur, providing businesses with accurate information on their available stock at any given time. The cost of goods sold, inventory, and gross margin shown in Figure 10.15 were determined from the previously-stated data, particular to perpetual FIFO costing. The specific identification costing assumption tracks inventory items individually so that, when they are sold, the exact cost of the item is used to offset the revenue from the sale.

Using a perpetual system, it has real-time information about which site may have one in stock so the customer can go get his wrench quickly instead of driving from store to store looking for it. Even though GAAP standards say that either perpetual or periodic systems are appropriate for any business, each is more suited to different-sized organisations. Overall, perpetual systems are more suited to companies that have high sales volume or multiple retail locations because it is a timelier system. Periodic systems could hinder decision-making for these types of organisations. Periodic systems are more suitable for businesses not affected by slow inventory updates.

At the time of the second sale of 180 units, the LIFO assumption directs the company to cost out the 180 units from the latest purchased units, which had cost $27 for a total cost on the second sale of $4,860. Thus, after two sales, there remained 30 units of beginning inventory that had cost the company $21 each, plus 45 units of the goods purchased for $27 each. Ending inventory was made up of 30 units at $21 each, 45 units at $27 each, and 210 units at $33 each, for a total LIFO perpetual ending inventory value of $8,775. The specific identification method of cost allocation directly tracks each of the units purchased and costs them out as they are sold. In this demonstration, assume that some sales were made by specifically tracked goods that are part of a lot, as previously stated for this method. For The Spy Who Loves You, the first sale of 120 units is assumed to be the units from the beginning inventory, which had cost $21 per unit, bringing the total cost of these units to $2,520.

Regardless of which cost assumption is chosen, recording inventory sales using the perpetual method involves recording both the revenue and the cost from the transaction for each individual sale. As additional inventory is purchased during the period, the cost of those goods is added to the merchandise inventory account. Normally, no significant adjustments are needed at the end of the period (before financial statements are prepared) since the inventory balance is maintained to continually parallel actual counts.

Notice the cost of inventory and COGS are different under the perpetual and periodic inventory systems since the goods sold come from different LIFO layers. In a periodic inventory system, you only update the inventory account at the end of the period, such as monthly, semiannually, or annually, after a physical inventory count. The basic concept underlying perpetual LIFO is the last in, first out (LIFO) cost layering system. Under LIFO, you assume that the last item entering inventory is the first one to be used.